Restaurants deal with perishable food items daily. Maintaining inventory properly is thus an important part of managing a restaurant. Poor restaurant inventory management can increase the overall operational costs and cause a dent in your profits. In the food and beverage industry, keeping track of customer demand is essential to avoid overstocking or understocking. Inventory management helps companies optimize their food cost percentage and ensure that ingredients are fresh and readily available. Additionally, managing inventory effectively can aid in cash basis accounting, which simplifies the tracking of payroll taxes and other expenses.

Inventory accounting for restaurants comes in as the savior. It is as important for a restaurant to maintain proper inventory accounting records as any other task. As a restaurant operating in the USA, your biggest challenge is to satisfy the customers while managing the restaurant costs. Restaurant inventory accounting can be your biggest aid to balance this out.

As per a report, around 58% of restaurant owners in the USA were highly concerned about the rising cost of operations and the impact it would have on their bottom line, especially post-pandemic. Inventory accounting for restaurants is an effective way to manage your financial health.

With restaurant inventory accounting, you can usually ensure the following:

Budget your operating expenses and manage orders accordingly

Reduce the burden of taxes by using the best accounting methods

Increase your profitability

In this blog, we take a holistic view of inventory accounting for restaurants and how it can make your overall inventory management more robust.

What is the importance of Inventory Accounting for Restaurants?

As a restaurant owner, you might ask, why should you opt for inventory accounting for restaurants? You need to implement proper inventory accounting to keep your restaurant financially stable. Here are the reasons:

Impact on the Overall Financial Health of the Restaurant

Focusing on restaurant inventory accounting, you can ensure good financial health by:

Calculating Profitability

Inventory accounting calculates the Cost of Goods Sold (COGS).

It shows the actual cost of the items you sell in your restaurant.

Accurate measurement of COGS using inventory accounting can:

Help you manage and reduce the cost of material.

Set appropriate prices in the menu.

Avoid over or underpricing the food items.

Improve your profitability.

Reduce food cost and food cost percentages.

Budgeting Expenses

Having detailed records of the food inventory helps you to predict future fixed costs.

You can manage your purchases strategically so that there is proper financial planning.

It also helps you prevent overstocking or understocking of material.

Control your prime costs.

Tax Planning

There are three ways of calculating inventory, namely, FIFO, LIFO, and weighted average cost.

You can use these methods to save taxes by reducing your profits for a period.

Inventory Management with Inventory Accounting

Is there a connection between inventory management and inventory accounting for restaurants? Let’s find out how:

Effective Inventory Management

To manage inventory effectively, you must track the purchased, used, and wasted ingredients.

Inventory accounting gives you the necessary tools to manage inventory by performing:

Regular inventory counts.

Inventory aging and movement tracking.

Waste recording and management.

Effect on Financial Statements

By maintaining regular records using efficient restaurant accounting software, you can ensure:

Effective Inventory Management.

Accurate Financial Statements.

Reflection of true costs.

Increased profitability.

You can identify opportunities to save and reduce your Cost of Goods Sold (COGS) by, maintaining proper records.

Inventory and food waste management are the biggest operational challenges faced by restaurant industry. Inventory accounting can help you solve this issue.

Understanding the Basics of Inventory Accounting

Before you implement restaurant inventory accounting, it is important to understand all the basic concepts including fluctuating food costs, vendor management, and the impact of labor costs on net profit. By understanding the purpose and outcome of each of these concepts you can make informed decisions to manage inventory effectively. These decisions affect everything from food sales and restaurant expenses to labor costs, which in turn influence your net profit. By grasping these dynamics, you’ll be better equipped to optimize your restaurant’s operations.

Key Concepts of Inventory Accounting

Cost of Goods Sold

COGS is the cost of ingredients and raw materials used by a restaurant.

Your restaurant’s COGS will vary based on these factors:

The price of ingredients.

Time of procurement.

Inflation.

Seasonal changes in the availability of raw materials.

Venue of your restaurant.

Quality of food you serve.

Type of meals you offer.

Quantity of items.

Types of cuisines that you serve.

Whether you operate a small restaurant or a five-star restaurant.

Ideally, you should maintain a COGS of around 30% to keep your finances healthy.

Put simply, it is the most important operational cost for a restaurant.

Valuation Methods

FIFO (First in, First Out): The FIFO method is used to calculate the inventory value when the items are used chronologically, i.e. items purchased first are used first.

LIFO (Last in, First Out): The LIFO method is used to calculate the inventory value when the latest items purchased are used first.

Average Cost: It is mostly used when the prices are highly volatile and it is impossible to keep track of each purchase or sale separately. In such a case, the total cost per unit is averaged out.

Inventory Turnover Ratio

-

It shows the rate at which inventory is used and replaced with fresh items.

-

The Inventory Turnover Ratio is useful in the movement analysis of the inventory.

-

If the value of this ratio is high, it shows efficient inventory management and vice versa.

Impact of Inventory Accounting Concepts on Financial Statements

Now let’s see what impact these key concepts of inventory accounting for restaurants have:

Cost of Goods Sold

Once you accurately calculate your COGS, you can:

Price your dishes appropriately for every event and occasion.

Increase the profitability of your restaurant business.

Predict future costs and plan well in advance to avoid a cash crunch.

Valuation Methods

You can use different inventory valuation methods to manage your tax liabilities. The valuation method can increase or decrease the COGS affecting the taxable income. Here’s how:

Price your dishes appropriately for every event and occasion.

In a market where prices are reducing, using FIFO can reduce your taxable income.

Using LIFO to value inventory in a rising market can reduce your tax burden.

Weighted Average cost is an all-weather method.

Inventory Valuation Methods for Restaurants

Having learned about the basic concepts of restaurant inventory accounting, you must have noticed the importance of inventory valuation. Let’s dive a bit deeper and understand each of the methods in some depth:

FIFO Method (First In, First Out)

Just like when we stand in a queue, everyone gets to enter in their respective order. The FIFO method of inventory accounting uses the same concept. Usually, the materials in a restaurant are used on a FIFO basis as they are perishable. Hence, FIFO is the most suitable method for restaurant inventory accounting. Here are the pros and cons of using the FIFO method:

Pros

FIFO reflects how the ingredients are used in a restaurant.

It provides the most accurate depiction of COGS in a restaurant, as it tracks the materials used to the T.

It is simple to understand and implement.

Cons

In times of inflation, you cannot save taxes using FIFO as the inventory used first is comparatively cheaper.

Example

Let’s take an example to understand how the FIFO method affects a restaurant’s inventory accounting.

Particulars | Rate | Amount |

Purchased 100 units of Item A | $ 50 per unit | $ 5,000 |

Purchased 500 units of Item A | $ 53 per unit | $ 26,500 |

Purchased 100 units of Item A | $ 60 per unit | $ 6,000 |

Total Inventory Purchases 700 units of A | $ 37,500 | |

Used 200 units of Item A (FIFO) | 100 units @ 50 and 100 units @ 53 |

(-) $ 10,300 COGS |

Closing Balance 500 units | $ 27,200 |

As per the FIFO method, you can see in the above example that the item purchased first is used first.

LIFO Method (Last In, First Out)

The LIFO method assumes that the items purchased last are used first. Practically, it is not possible to implement LIFO on perishable items. Hence, the LIFO method is used in restaurant inventory accounting to manage tax liabilities. Here are the pros and cons of using the LIFO method:

Pros

The LIFO method helps in saving taxes as the highest-priced inventory is assumed to be used first.

Especially, in times of high inflation, it can be really effective in reducing the tax burden.

It matches the current costs and revenues.

Cons

Implementing LIFO for actual physical inventory flow is impractical, especially in restaurants that use highly perishable items.

It never reflects the inventory costing held by the restaurant.

Using LIFO, your Balance Sheet might carry the cost of inventory already used for years.

Example

Let’s take an example to understand how the LIFO method affects a restaurant’s inventory accounting.

Particulars | Rate | Amount |

Purchased 100 units of Item A | Rs. 50 per unit | Rs. 5,000 |

Purchased 500 units of Item A | Rs. 53 per unit | Rs. 26,500 |

Purchased 100 units of Item A | Rs. 60 per unit | Rs. 6,000 |

Total Purchases 700 units of A | Rs. 37,500 | |

Used 200 units of Item A (LIFO) | 100 units @ 60 and 100 units @ 53 | (-) Rs. 11,300 COGS |

Balance 500 units | Rs. 26,200 |

As per the LIFO method, you can see in the above example that the item purchased last is used first.

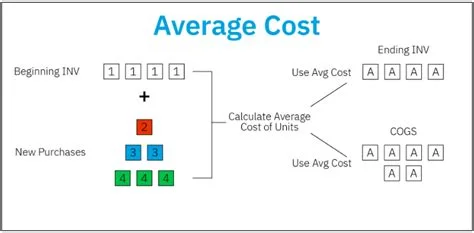

Average Cost Method

Unlike the FIFO or LIFO method, the average cost method calculates the average cost per unit of the inventory. This rate is applied to all the usage of goods. Although it doesn’t show the correct cost of the inventory, it is much more logical than LIFO and is easier to implement. Hence, the average cost method is also popularly used in inventory accounting for restaurants.

Here are the pros and cons of using the average cost method:

Pros

You can run inventory management system smoothly irrespective of inflation as the effect is evenly distributed.

Using average inventory costs makes inventory accounting for restaurants simpler.

Cons

Similar to the LIFO method, the average cost doesn’t represent the actual cost of inventory held by the restaurant.

The average cost method doesn’t depict the physical flow of inventory.

Matching the cost of inventory becomes difficult using the average cost method.

This can lead to rounding off balances as averages are most likely in decimals.

Example

Let’s take an example to understand how the average cost method affects a restaurant’s inventory accounting.

Particulars | Rate | Amount |

Purchased 100 units of Item A | Rs. 50 per unit | Rs. 5,000 |

Purchased 500 units of Item A | Rs. 53 per unit | Rs. 26,500 |

Purchased 100 units of Item A | Rs. 60 per unit | Rs. 6,000 |

Total Purchases 700 units of A | Rs. 53.57 per unit | Rs. 37,500 |

Used 200 units of Item A (Average Cost) | 200 units @ 53.57 per unit | (-) Rs. 10,714 COGS |

Balance 500 units | 500 units @ 53.57 | Rs. 26,785 |

By normal subtraction, the amount of balance units comes to Rs. 26,786 (37,500 – 10,714). As you can see the average cost method has reduced the balance by Rs. 1, causing a rounding-off error. However, it can be cured by using accurate inventory software that records all the decimal values. | ||

As per the average cost method, you can see in the above example how the average cost is taken for restaurant inventory accounting.

You must have noticed how the COGS changes while using different methods for the same data, i.e.:

FIFO Method: Rs. 10,300 (Lowest).

LIFO Method: Rs. 11,300 (Highest).

Average Cost Method: Rs. 10,714.

The COGS is the highest in the LIFO method, leading to lower taxable income and saving taxes.

Most Popular Inventory Valuation Method

When choosing the right valuation method for restaurant inventory accounting system, consider these points:

Does the valuation method fit the:

Type of restaurant.

Pricing strategy.

Financial goals.

Type of ingredients you use.

The inventory valuation method should give a clear picture of the actual position of your inventory.

The FIFO method is more suitable if you want the accurate cost of the ingredients

The LIFO method aids in tax saving by increasing the COGS

Restaurants use the average cost method for a more simplified and steady approach.

FIFO Method: The most popular inventory valuation method is FIFO. Restaurants around the world prefer the FIFO method for accurate restaurant inventory valuation because of these advantages:

It shows the natural flow of inventory.

Reflects the accurate COGS.

Aids in proper pricing of menu items.

It is simple to understand and implement making it easier for the staff.

Easily manage and track stock movement.

Identify and reduce the cost of slow-moving items.

It shows the correct profits of the restaurant making your books more reliable.

How to Implement Inventory Accounting Practices?

Now that we are done with all the basic concepts, it is time to understand how you can implement inventory accounting for restaurants.

Maintain Proper and Accurate Inventory Records

You should ensure that the inventory is properly recorded. To achieve this, you should apply processes for the following:

Purchases: Here are the things you should check for recording purchases properly:

Keep a record of the purchase orders raised.

Maintain the documents related to the deliveries received.

Cross-check if the deliveries match your purchase orders.

Verify the quality and quantity of the ingredients.

Storage: A restaurant needs to store the inventory well as it is highly perishable. Here’s the checks you need:

Whether the storage is properly labeled to ensure the inventory is stored in the right places.

Goods that need cold storage are managed accordingly.

The storage area is accessible to trained staff to avoid losses and wastage.

Usage: Recording the usage is the most crucial stage in inventory accounting for restaurants. Keeping a proper record of usage helps to know the correct COGS and price the items appropriately. Here are the points to track:

Keep a daily tracker to monitor the usage.

Analyze the movements of each ingredient and make tweaks if necessary.

Proper measuring tools to optimize the usage and minimize wastage

Ensure that goods entering first are used first

Spoilage: Track these things to record wastages:

Document the reasons for the spoilage

Also, document the employee’s name involved

Was it avoidable or unavoidable

What measures can be implemented further to reduce waste and spoilage

Use Inventory Management Software

While the above task might look daunting at face value, it can become much easier and more convenient with the help of inventory management software. Here are the benefits of using software to maintain inventory accounting for restaurants:

Automated Data Entry: The software can record purchases automatically on delivery or with minimum manual intervention. This can reduce the efforts and risk of errors.

Reporting: Using software, you can generate crucial inventory reports and get the COGS calculations in no time. It can help you make quicker pricing decisions.

Integrate with Accounting Software: You can easily share data between the inventory and accounting software to reduce data redundancy.

Fewer Errors: Using software helps you reduce the chances of manual errors.

Quick Decision Making: Aided by proper information, on time, you can make faster decisions increasing your efficiency.

Implementing inventory accounting for restaurants has many benefits including, good financial health, proper budgeting, reduced waste, optimum utilization of resources, and proper inventory management. You should learn the basic concepts and apply restaurant inventory accounting to make the processes more efficient.

Frequently Asked Questions

You can implement inventory accounting for restaurants to maintain proper records. It can help you track the purchases, usage, wastage, and inventory movement. By recording the proper cost, you can price your menu items appropriately and enjoy good profits.

FIFO (First In, First Out) is the best method for inventory valuation in restaurants. It provides the correct representation of the inventory as restaurants use perishable items that are used on a FIFO basis.

Restaurants should use specialized software for inventory accounting and management. Using software along with spreadsheets can help in the proper tracking and management of inventory.

You can use this formula to calculate the value of inventory:

Cost of Goods Sold (COGS) = Opening Inventory + Purchases – Closing Inventory

You can maintain the proper records of inventory to know the opening balance, purchases, and closing balance. The balancing figure is the COGS.